A Better Emergency Fund?

Building a simple "inflation proof" emergency fund

It has always been said to keep your emergency fund in a safe savings account where it cannot drop in value. This makes sense for safety and liquidity, but there is a major drawback: your money is likely losing value to inflation. If your savings account earns 2% and inflation is 3%, your emergency fund is actually shrinking every year.

However, you can invest your emergency fund in a way that aims to beat inflation while remaining relatively stable, or even more stable than just cash.

The Strategy: The 90/10 Split

The goal of this strategy is to keep the majority of your money safe while using a small portion to drive growth so that your emergency fund can outpace inflation. What I’ll be writing about is a strategy that invovles 90% in cash-like assets and 10% in stocks.

The 90% (Safety): This portion ensures that most of your money is there when you need it and protects against market volatility.

The 10% (Growth): This small slice acts as an equity kicker to help the portfolio grow over long periods so you do not have to keep topping it off manually to keep up with rising prices.

One way to manage the risk of a severe market drop is to overfund the account by the amount you have in equities, or in this case, 10%. Let’s say your emergency fund covers 3 months of expnses, and for you that is $10, 000. You could aim to save $11,000 with $10,000 being in cash-like assets and $1,000 in stocks. This is an optional step, but it provides a cushion so that even if the stock portion drops, you still have your core $10,000 available, and could also make you feel less stressed about your emergency fund during both good and bad times.

Long-Term Returns

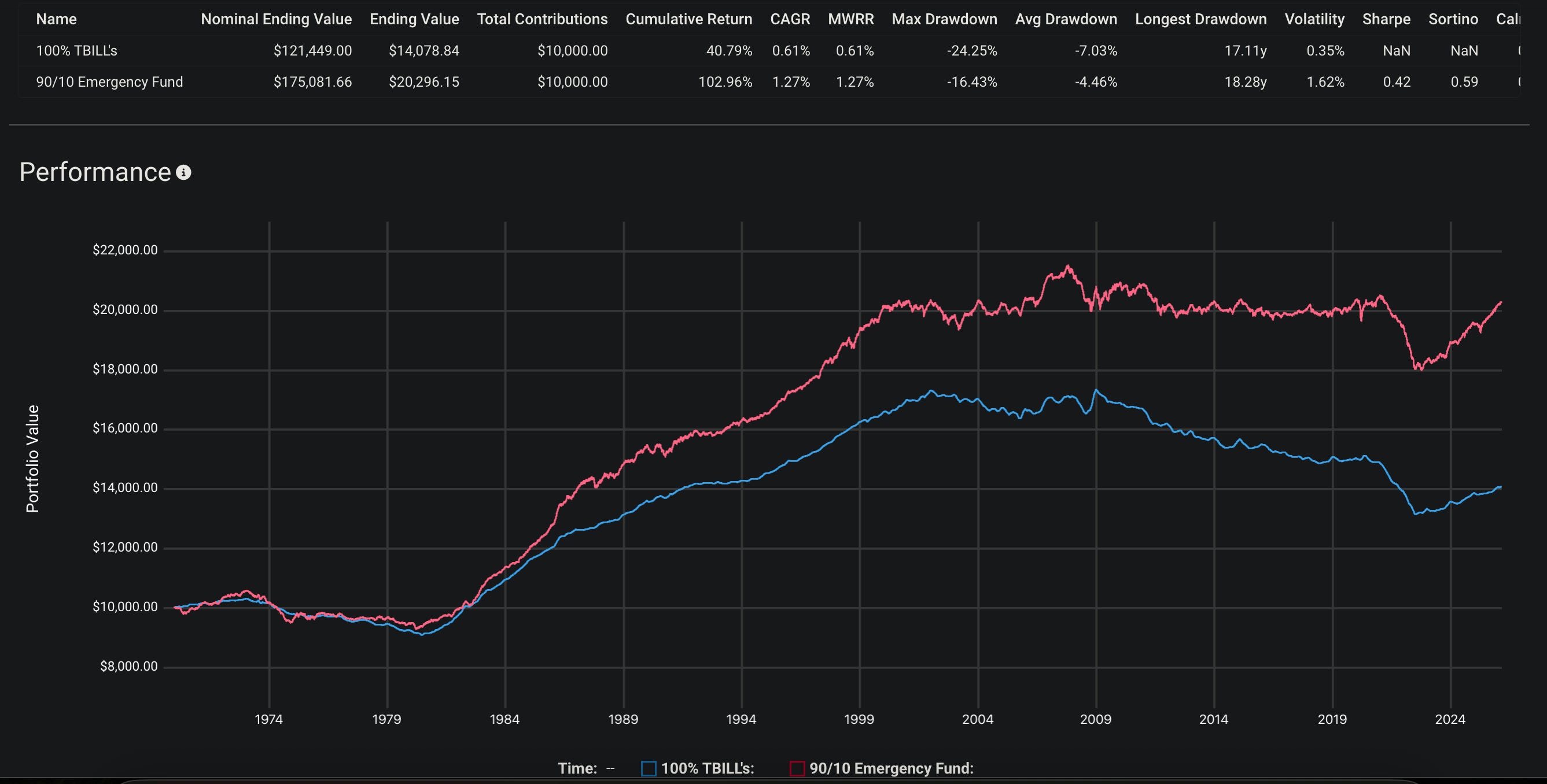

To see why this works, we can look at backtested data from December 31, 1969, through February 25, 2026. In this backtest, “cash” is represented by T-Bills, and “equity” is represented by a market-cap-weighted global stock market index fund from Vanguard.

When we adjust these returns for inflation, the difference between pure cash and a 90/10 split becomes clear.

As shown in the performance chart, a 10% tilt toward global stocks resulted in a much higher return compared to just holding T-Bills.

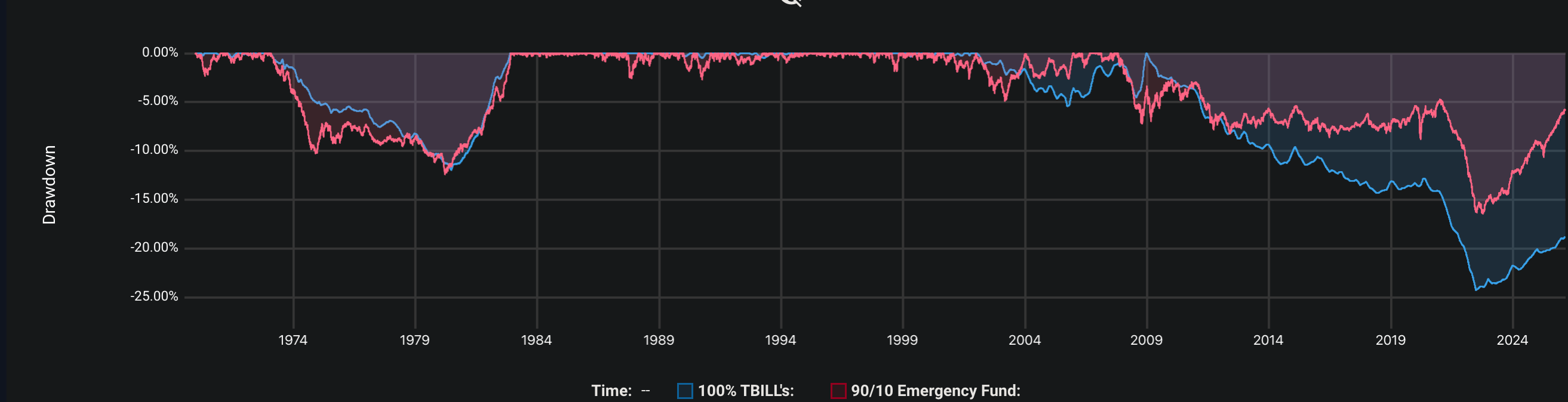

It is also important to look at drawdowns. While the 90/10 portfolio seems to experience more price movement than cash, the risk is often smaller than people realize. Even during major market crashes, the total impact on the portfolio is limited because 90% of the fund remains in stable assets. Being in cash had both a higher max drawdown, and higher average drawdowns.

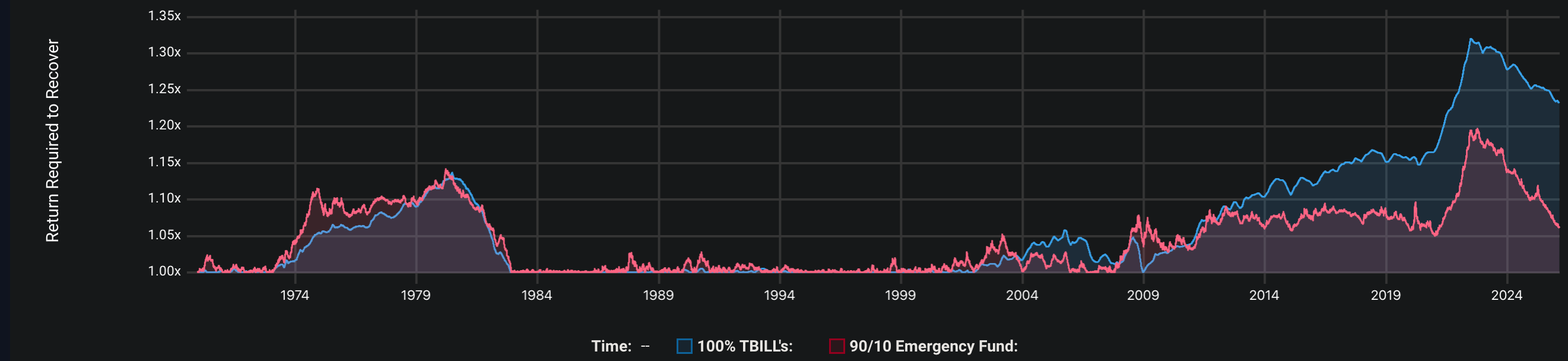

Because the drawdowns for a 90/10 portfolio are typically shallow, the return required to get back to even is very low.

How to Build the 90% Base for Canadians

For the 90% portion, you want assets that are stable and easy to access. In Canada, you have several strong options:

High Interest Savings Accounts (HISA): These provide the best liquidity and same-day access to your cash. You can use the HighInterestSavings.ca chart to find banks offering the highest rates.

Money Market ETFs (ZMMK or CASH): These ETFs typically offer higher yields than traditional bank accounts. They are very stable but require one business day for trades to settle before you can withdraw the cash.

T-Bill ETFs (CBIL): This ETF holds short-term Government of Canada Treasury Bills and is one of the safest places to park cash in the Canadian market.

Cashable GICs: These offer a guaranteed interest rate but allow you to withdraw your money early if an emergency happens.

How to Build the 10% Growth Kicker for Canadians

For the 10% portion, the simplest approach is a broad global stock market ETF. Total Market ETFs (ZEQT or CAGE): These are low-cost, all-in-one funds that hold stocks from Canada, the US, and international markets. They handle all the rebalancing for you so your 10% allocation stays on track. If one wants even less risk, they can invest in a different asset allocation ETF that also holds bonds.

Rebalancing

To keep your emergency fund effective, you need to ensure the 10% equity slice doesn’t grow so large that it exposes you to too much risk, or shrink so much that you lose your inflation protection.

It is probably best to just rebalance once a year to fix your allocations.

Once a year, review the total balance of your fund. If your stocks have grown significantly (for example, to 15% of the total), sell the excess and move it into your HISA or money market fund. This effectively “locks in” your market gains into the safe portion of your safety net. If a market downturn has reduced your equity portion to 7% or 8%, move some cash from your 90% base into your global ETF, or direct new savings to your emergency fund’s etf.

Conclusion

Investing your emergency fund is a personal choice. It may be best suited for people with stable jobs and no high-interest debt. By using a 90/10 split and focusing on high interest savings and global stocks, you can protect your savings from being eroded by inflation while keeping your safety net intact.

You can view the full 50-year backtest and data used for this article here: https://testfol.io/?s=aZLYJSI8JSR